Wind and solar in Spain – Overview of 2021

For the fourth year, we publish the summary of how wind and solar have performed in Spain in the year just ended. Although the final stretch of the year has been marked by the incredible escalation in electricity prices, in 2021 many relevant things have happened related to renewables in Spain: second renewable auction, offshore wind and self-consumption roadmap, renewable PERTE, etc.

The raw data for this report are publicly available on Entso’s excellent website and on REE’s very complete Esios portal.

1. Electricity generation mix

According to REE data, wind was the main source of electricity generation in Spain in 2021, accounting for 23.3% of the mix. It is followed at a considerable distance by nuclear with 20.6% and it is very relevant that solar PV already accounts for 8.1%.

Beyond the anecdote, the important thing is that wind and solar are the sources that are growing the most compared to 2020, although this still seems a slow pace if we want to meet the 2030 targets.

2. Daily production

- As usual when viewing this type of graph with daily resolution, it is impressive to see the great variability of wind power production, with peaks and valleys that follow one another in the space of hours. With battery systems now available with storage capacity of 4h at Lion and more than 8h at flow, the year is getting closer and closer when these saw-toothed peaks will disappear and will not be a grid integration problem.

- Wind generation reached its daily maximum on December 8, with 416 GWh of production. That day also saw the maximum combined wind+solar production of almost 450 GWh.

- Solar PV, on the other hand, reached its maximum production on June 29 with almost 125 GWh.

- As for the minimums, the variation ranges for wind and solar are quite similar, since in the case of wind the minimum is 4.5% of the maximum, while in solar it is 5.6%.

- If we consult in greater detail the generation structure of 8/12/2021, it can be seen that at 15:00h, wind and solar covered 72% of the demand, leaving the contribution of gas and coal at a meager 3%.

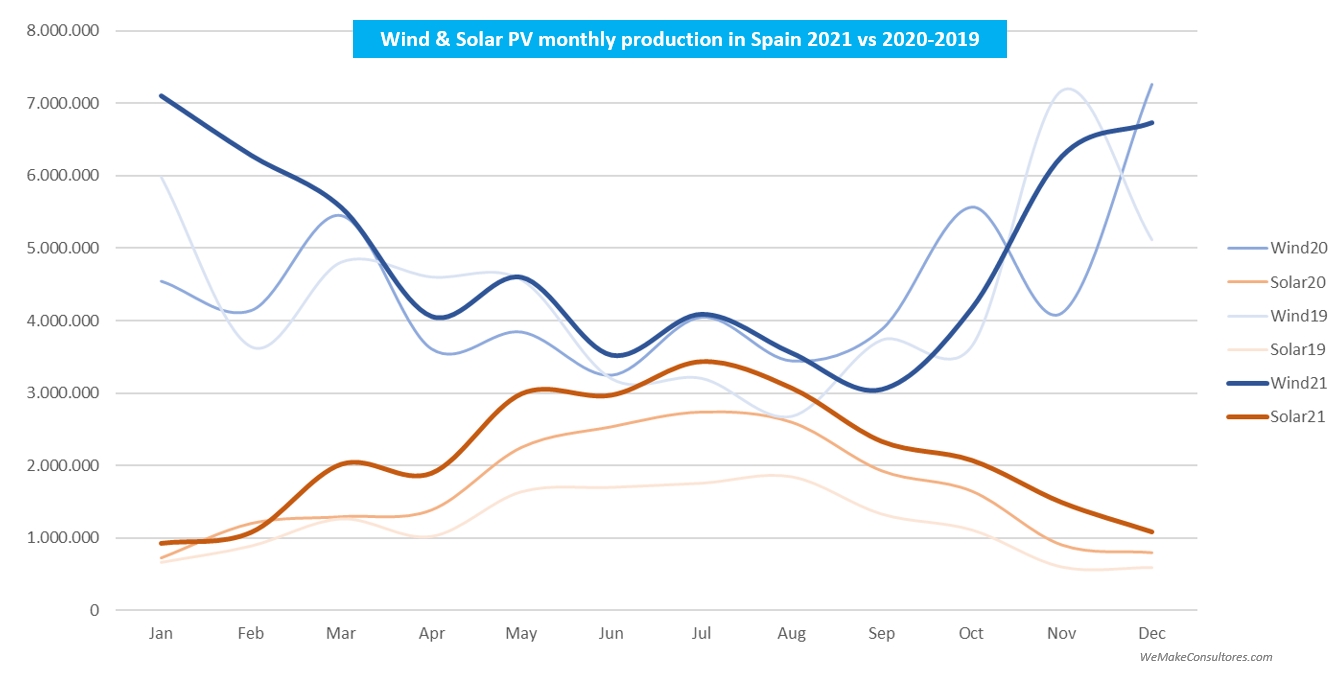

3. Monthly production evolution

- By representing the production data by month, the curves are much smoother and the great seasonal complementarity of wind and solar is much better appreciated.

- It is likely that in 2022 we will see solar over wind for the first time in some summer months.

4. Annual production evolution

- Solar PV was once again the main protagonist in 2021 due to its strong growth in annual production, although this year wind also grew by over 10%.

5. Installed capacity

- In terms of installed capacity, there is still no definitive data, but taking the data published by REE on its website, we can see that photovoltaic has grown by almost 3GW, which is in line with the PNIEC’s objectives. However, wind has only increased its capacity by 584MW, which is far from the 2GW/year path set by the PNIEC.

- This low level of wind installations is striking, as the auction and the queue of applications show that there is an appetite for investment, so it seems that the bottleneck is in the permitting process. This issue deserves an in-depth analysis in the future.

- As in recent years, the best news is that the coal generation fleet continues to be decommissioned, with 2GW retired in 2021.

6. Capacity factor

- In terms of capacity factor, solar PV remains stable at 20% while wind returns to values of 24% not seen since 2018

- It should be remembered that the main element affecting the capacity factor is the resource (wind and irradiance) available each year, but there are also other factors such as technology efficiency, maintenance or curtailments. In general, with equal resource we should see better capacity factors as both solar and wind technology is becoming more efficient.

7. Market prices and renewables

- And we come to the big protagonist of the last months of 2021 (and unfortunately will continue to be so in 2022): wholesale market prices. If exactly one year ago we were talking about the fact that 2020 had set records in low pool prices due to the drop in demand due to covid-19, now we are talking about the exact opposite: record high prices. December’s average price of almost 240 €/MWh was unimaginable just a few months ago.

- We are not going to analyze here the causes of this escalation as there are many (and some, the less, very good) analyses available of what is happening, but I think we should get used to this price volatility as we are in the middle of the transition of the energy model and tensions are inevitable. Let’s hope that the regulatory framework is flexible and fast enough to adapt to this transition and does not increase the imbalances inherent in the process.

2021 has been a good year for renewables. Wind power has been the main source of generation in Spain, solar power has reaffirmed its position as the fastest growing and most promising source, renewable auctions have been successfully established, offshore wind regulation kicks off, self-consumption and energy communities are picking up speed…

We are moving in the right direction, but let’s not deceive ourselves: we need more speed or we will not meet the 2030 targets. We need to speed up the project pipeline while increasing the positive impact of projects on local communities, offshore wind timelines need to be accelerated, and storage needs to be a priority.