Analysis of the second renewable auction in Spain

On 19 October, the second renewable auction was held in Spain with 3300MW of capacity up for bidding. There was a lot of expectation to see the results as it was held in the middle of the storm over the wholesale price of electricity and the dispute between the government and utilities.

In this article we review the most important elements of the results of this auction

1) VOLUME AND QUOTAS

One of the great novelties of this auction were the new quotas for accelerated installation and distributed generation, but they have been the protagonists not precisely because of their success but because they have been practically deserted and it has been wind power that has covered them. The multi-technology quota has also been 100% covered by wind power, which is also unusual.

This failure with the new quotas has been one of the big surprises and among the multitude of post-auction analyses, we highlight several possible reasons:

- It seems that the non-public price cap may have been one of the main reasons, especially for distributed generation.

- It is also clear that companies go to the auctions to secure capacity but with very immature projects. This is perhaps why the accelerated installation quota has been so unsuccessful.

- In the distributed solar generation quota, the lack of specialised developers may also have had a negative influence.

Another notable fact has been the greater success of wind compared to solar. This may have to do with greater uncertainty and exposure of solar projects to rising costs as much of the supply chain is in China.

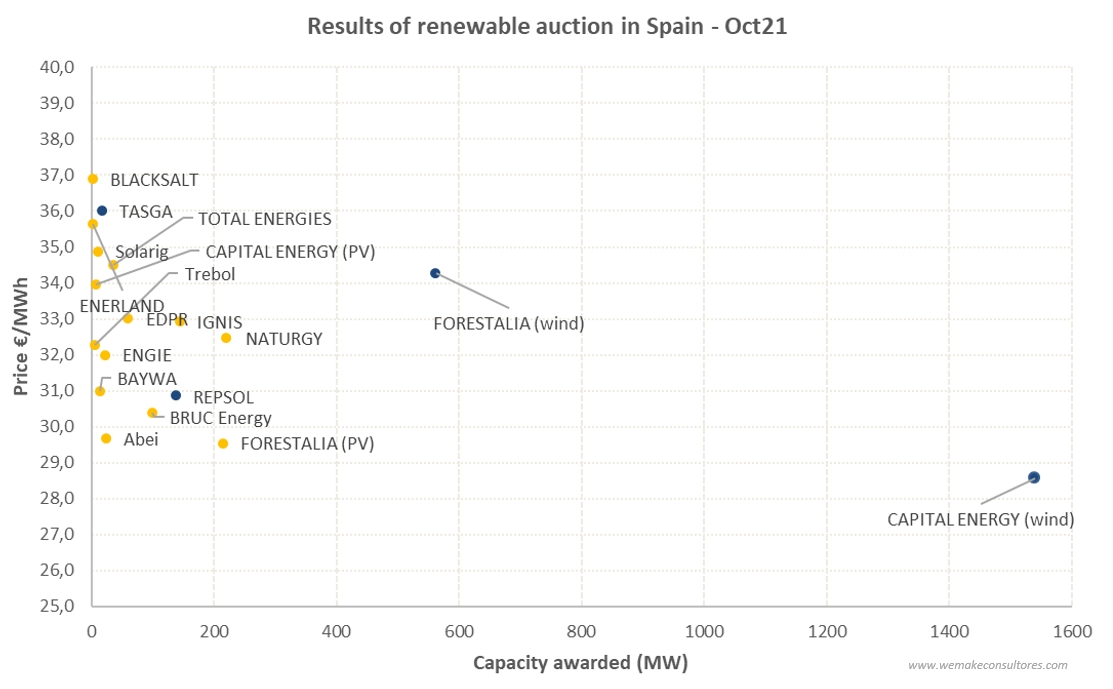

2) PRICES

Prices have been more than 5€/MWh higher on average than the first auction. Very striking that the weighted average price of wind (30.18 €/MWh) has been lower than that of solarPV (31.64 €/MWh).

Source: AEE

- The higher prices were expected and foreseeable due to the generalised rise in costs, rising PPAs and very high pool prices. The same is happening in other auctions, such as the recent one in Colombia, where the price for solar PV went from $25/MWh two years ago to $41/MWh.

- The solar and wind prices are stranger as the capex of solar PV is still lower than that of wind, but it seems that supply problems and rising prices are affecting solar more and could be an explanation. Rystad recently published an article warning of the impact of the current situation on the viability of solar projects.

3) WINNERS

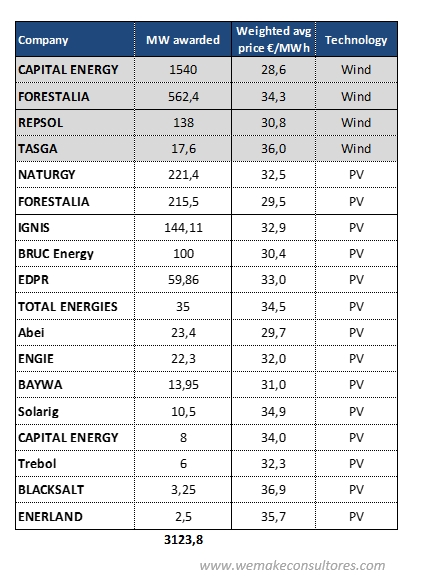

Capital Energy and Forestalia are the big winners, but it is striking that there are fewer bidders than in the first auction (16 vs 27), as well as the significant absences of Iberdola, Acciona, Enel, Greenalia and Solaria, among others.

- The big utilities’ pressure on the government due to the Royal Decree that cuts their profits has probably influenced the lower number of participants, but I don’t think this is as much as has been said, for several reasons:

- Large utilities have never been fans of auctions, as Iberdrola’s CEO Sanchez-Galán said a few months ago, as they introduce additional competition to their business, since large utilities can finance themselves with their own resources and obtain internal and external PPAs more easily than small developers, who with auctions are able to secure part of their revenues and thus facilitate financing.

- Naturgy, EDPR and Engie have attended, meaning that the major absentees are “only” Iberdrola, Acciona and Enel.

- In addition, the very high pool prices were not an incentive to go to the auction and even less so for large utilities that have other options, so it does not seem to have meant much sacrifice to “stand up” to the government.

- Forestalia (wind), Naturgy (solar) and Ignis (solar) have obtained the best prices with very significant volumes.

- Although the distributed generation quota has been almost deserted, Enerland and Blacksalt have been the only bidders.

In short, there is still an appetite for securing revenues via auctions, but it will be necessary to design the next auctions better if these competitive processes are to serve to promote new avenues of development such as distributed generation. Although award prices have increased, on days when the pool exceeds €200/MWh, talk of generation plants that, even with rising costs, commit to prices of €30/MWh is very significant and provides clues as to the path to lower electricity prices in the medium term.

[Here the full analysis of FIRST renewable auction in Spain]