The state of the wind turbine manufacturing sector in 2026: a bipolar disorder

As we do every year, we’re gearing up for WindEurope 2026, which takes place in a few days’ time in Madrid, by reviewing the situation of the leading wind turbine manufacturers. How did 2025 go and what can we expect in 2026? Well, the short answer is that we are facing a sector that is clearly bipolar on two levels: between profitable and unprofitable manufacturers, as well as between the Chinese and Western markets… and everything points to this bipolarity continuing and even becoming more pronounced.

A look back at 2025: the differences are widening

Let’s start with the obvious: 2025 has been a good year… but not for everyone.

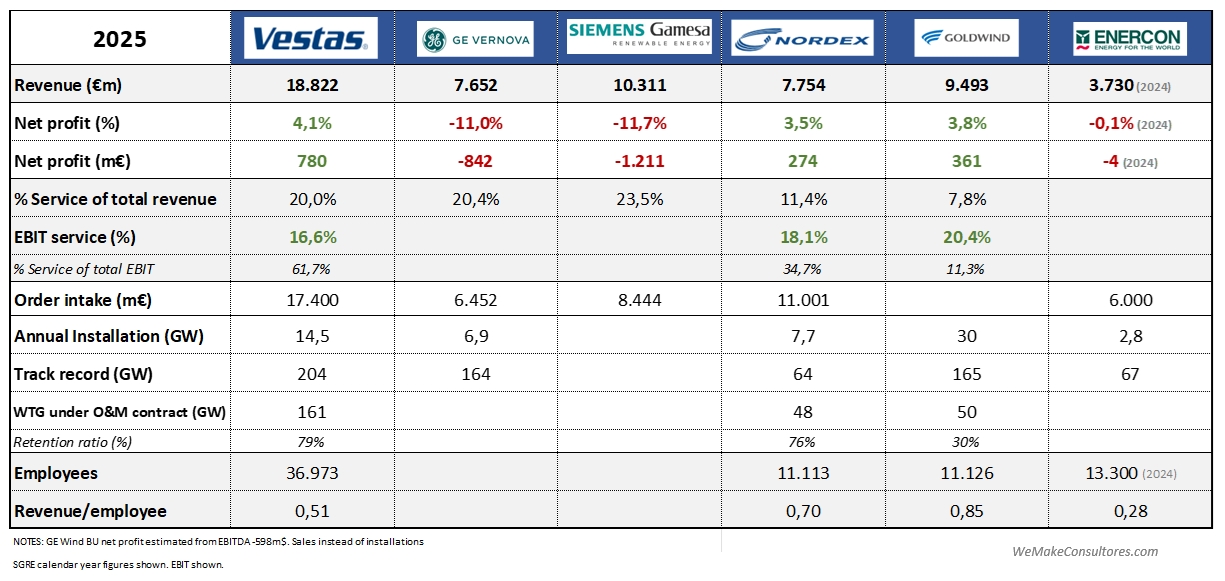

Vestas and Nordex are on the path to profitable growth, improving virtually all their indicators. Goldwind rounds off the group of winners with equally positive results.

But if these three OEMs are one side of the coin, we have the other side with Siemens Gamesa and GE Vernova, which for yet another year (and there have been quite a few now) have recorded losses running into millions in their wind power businesses. Although the situation has led some shareholders to call for more “drastic” measures, it is clear that the spectacular results from the rest of both parent companies’ businesses are breathing new life into the wind power business.

As for Enercon, although its figures are published a year late, it is good news that it has reached breakeven and, above all, that its order intake for 2025 has been very high, undoubtedly thanks to the high level of activity in the German onshore market.

As a point of interest, Vestas has become the first OEM to exceed 200 GW of installed capacity in its history, although at the current rate, we could see Goldwind join the club by 2026.

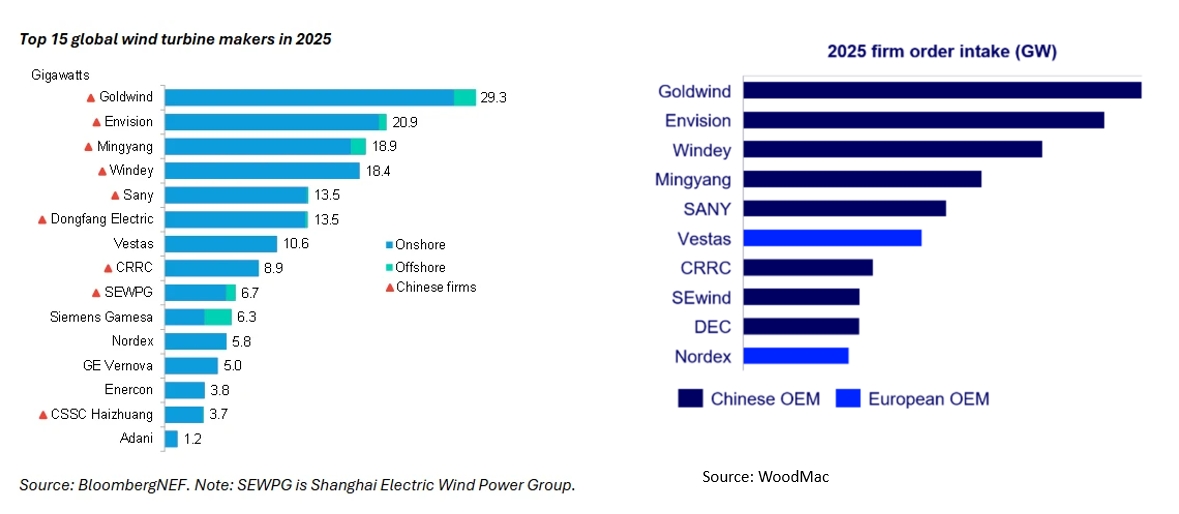

As for the global manufacturer rankings, there are few surprises, with the top five spots occupied by Chinese players. A few years ago, this would have made headlines, but today it is simply the logical consequence of a market that accounts for over 50% of the global total.

This is a clear illustration of the market’s bipolarity: over 50% of the market is in China, with its own dynamics, marked by a local supply chain, a fierce price war and a race to develop the largest turbines. On the other hand, there is the Western market, where profitability and reliability are finally prioritised over volume and size. These two markets are becoming increasingly different, making it very difficult for an OEM to compete in both at the same time. If we add trade barriers to this, the much-feared ‘Chinese invasion’ of Europe seems increasingly unlikely. The process of Chinese players entering Europe will require them to adapt their business to European dynamics, that is, with a local structure, adapted products and perhaps local manufacturing, and all this will take time and investment.

Financial performance

Analysing the quarterly trends in the key financial figures reveals some interesting patterns

- Revenue

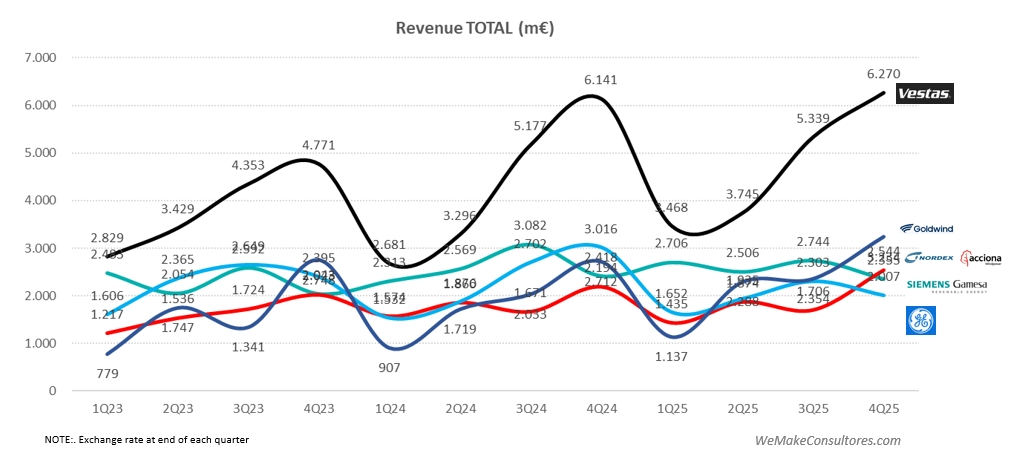

Revenue for the top five manufacturers grew by 4% in 2025 compared with the previous year. The significant gap between Vestas and the others is striking. Whilst Goldwind is the undisputed leader in terms of installed capacity, Vestas takes the lead in terms of revenue. The explanation lies in the vast difference between Western manufacturers and Goldwind in terms of revenue per MW installed. Whilst Western manufacturers are above one million euros per MW, Goldwind does not even reach a third of this figure. Chinese prices and the smaller scale of operations account for part of the difference, but this is something that requires careful analysis.

Nordex, for its part, has already surpassed the revenue of GE and SGRE in the last quarter, something unimaginable a few years ago.

- Profitability

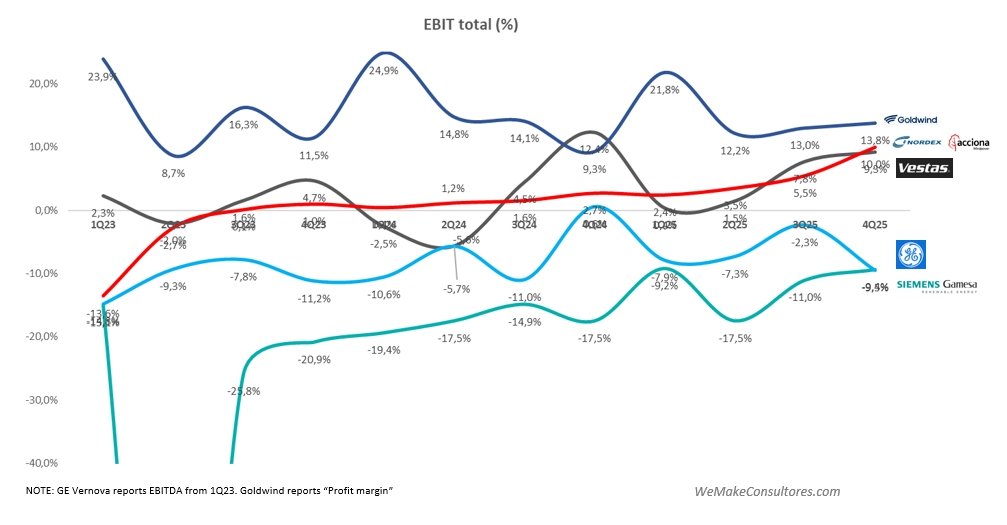

This graph clearly shows the other dichotomy we mentioned in the title. Whilst Goldwind, Vestas and Nordex remain in the black, GE and SGRE have yet to find their way back into profit. As we explained in the article on Nordex, although the recipe for recovery is well known, it is clear that execution is complex, and whilst Vestas and Nordex are nailing it, the others have yet to get it right.

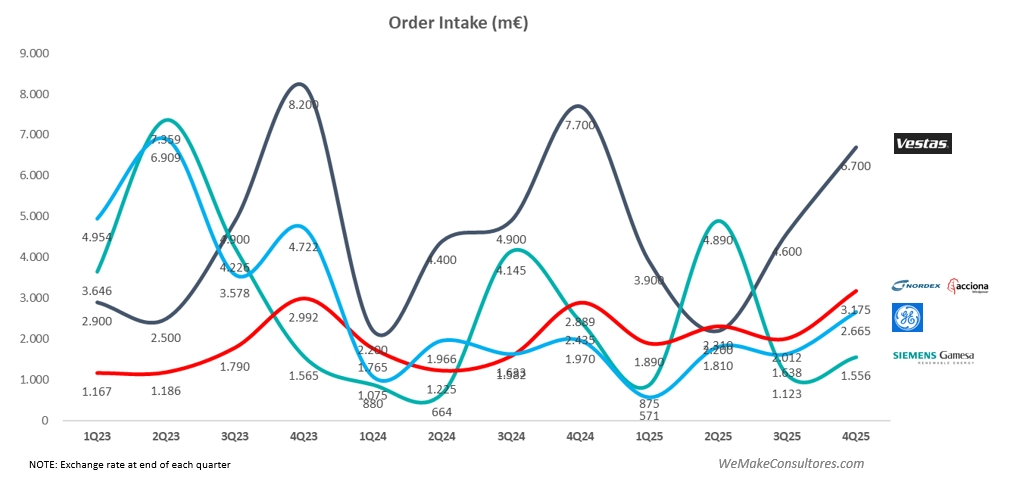

- Order intake

As for order figures, the annual data is very similar to that of 2024. The difference is that 2025 has seen higher onshore volumes, driven by the German locomotive which shows no signs of slowing down and has announced an extra 12 GW to be auctioned before 2030.

Offshore, however, is going through a rough patch. In Europe, 40% fewer contracts have been signed than in 2024, and in the US, the situation is well known. The UK’s Allocation Round 7 has been the best news of the year, as it generates a new pipeline for the coming years.

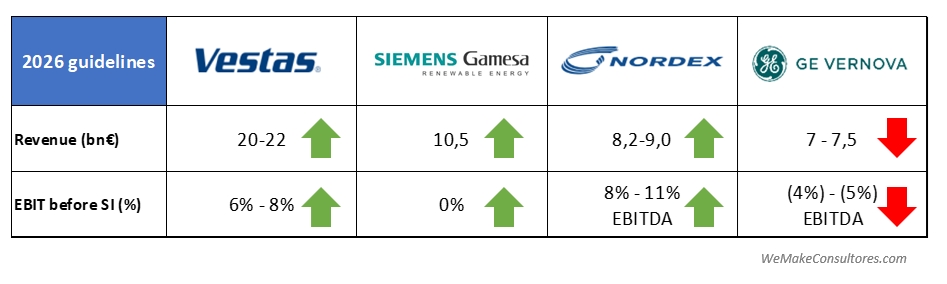

What does 2026 look like?

If we look at the forecasts published by the companies themselves, we see that Vestas and Nordex are confident of continuing on the right track in 2026, with growth in both revenue and profitability.

Siemens Gamesa, for its part, faces the major challenge of reaching breakeven this year, and the initial data gives cause for optimism. Undoubtedly, any strategic decision to divest all or part of the business depends on stabilising the unit, so breakeven is key to the future.

GE Vernova is the only one that sees no end to its problems. As it attempts to wind down its offshore operations in the least disastrous way possible, and with its onshore business heavily dependent on the vagaries of Trump, the outlook is not very optimistic.

Conclusions

- It is possible to grow whilst remaining profitable, as Vestas and Nordex are demonstrating

- The gap between OEMs is widening between clear winners and structural laggards

- The global market is becoming less and less global. China and the West are evolving according to completely different logics, and it is becoming increasingly difficult to compete in both with the same business model.

- Onshore is once again the driver of demand, whilst offshore is readjusting its business cases to the new reality.

- Topics to watch in 2026:

-

- Siemens Gamesa’s breakeven

- Chinese OEMs adapting to enter the European market

- How patient will GE Vernova and Siemens Energy remain with their wind power businesses?

- How long is the Chinese model sustainable?

energy-charts.info

energy-charts.info