Repoten 2: analysis of the major boost to wind repowering in Spain

On 22 May, the IDAE published the Provisional Draft Resolution for the second call for proposals under the “Circular Repowering” (REPOTEN 2) programmes. With €462 million on the table for wind power alone and 80 projects proposed for award, this represents the largest public investment in repowering that Spain has ever seen. We dedicate this month’s article to breaking down the figures and, above all, to attempting to answer the million-dollar question: what effect will this have on the sector?

The resolution in figures

Firstly, the basic data on the results of the call for proposals (focusing on Programme 1, wind power, which is what interests us):

- 80 projects proposed for funding in Table 1.1 (plus a waiting list of around 25 additional applications).

- 2,387 MW of capacity following repowering.

- 1,879 MWh of associated hybrid storage.

- €3,545 million in cumulative eligible costs.

- €462 million in aid granted, following the €220 million budget increase approved on 19 May (the initial allocation was €252 million for wind power).

- Average aid intensity: 13% of CAPEX, far from the maximum of 35%, which gives an idea of the level of competition that has existed.

- Average aid: €194,000/MW.

The implementation period runs until 30 June 2030, i.e. four years from the provisional decision. To be eligible, the wind farms must have commenced operation before 30 June 2010 (≥20 years old in 2030).

To put the volume into perspective, it should be noted that in 2025, 1,420 MW of new wind power was installed in Spain according to AEE (44 wind farms + 7 repowering projects), or 1,146 MW if we use REE’s figure. In other words, Repoten 2 Programme 1 alone mobilises 1.7 times the wind capacity that came on stream in Spain throughout 2025. Spread over the four years of implementation, this amounts to around 600 MW/year of repowering, equivalent to 40–50% of the annual rate of new installations.

This is not a marginal volume. It is a highly significant driver of demand for wind turbines, adding to the demand already generated by new projects.

How the projects were scored

In this call for proposals, it was necessary to balance the various criteria in the scoring system very carefully in order to achieve the highest possible score without forgoing too much funding. By analysing the average scores per criterion for the 80 winning projects, a number of conclusions can be drawn

It is clear that the technical, value chain and just transition criteria scored the highest for almost all projects. The administrative criteria were the truly tricky ones. The few projects that met them were able to request more funding and score lower on the economic aspect, whilst the rest engaged in a race to the bottom by requesting less funding in an attempt to improve their score.

In fact, the 10 projects with an Environmental Impact Assessment (EIA) achieved an average of 10.32 on the economic aspect, whilst the rest reached 20.46 – almost double. This explains the 13% aid intensity compared to the maximum 35% available.

The average score of 3.06 (out of 5) for public participation is surprising. It seems like an easy requirement to meet, yet only 60% of the successful applicants achieved it.

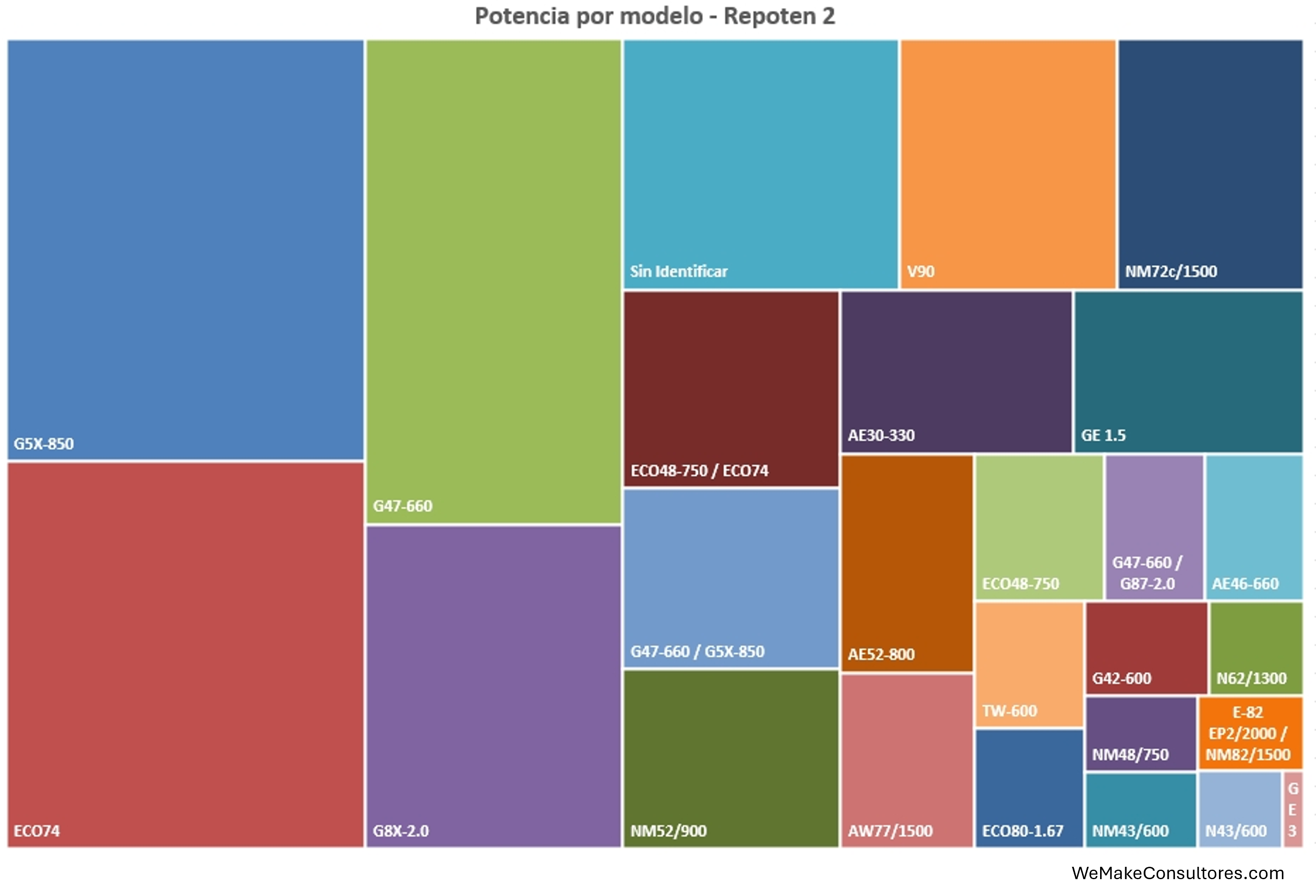

Which turbines are to be decommissioned?

If we look at the graph by model, the picture is quite telling:

The undisputed star is the old sub-MW guard that populated the Spanish countryside between the mid-1990s and the mid-2000s:

- G5X-850 (Gamesa, 850 kW): More than 400 turbines of this model alone.

- ECO7467 MW (Ecotecnia): almost 200 units to be decommissioned

- G47-660 (Gamesa, 660 kW): a further 430 turbines or so.

- And a long list of other models from MADE, Neg Micon, Tacke and others

Adding up all models below 1 MW exceeds 1,000 MW, almost half of the tender. Translated into physical turbines, this amounts to around 1,500 wind turbines that will disappear from the landscape (using the typical ratio from the first call for tenders, where each new turbine replaced seven old ones, the result would be some 200–250 modern turbines following repowering). A dramatic change.

And then there is the group of 2 MW turbines, which deserves a separate mention:

- Siemens Gamesa G8X-2.0: almost 200 MW.

- Vestas V90 (2 MW): 124 MW.

- A few hybrids featuring the G87-2.0 and Enercon E-82 EP2/2000.

In total, more than 330 MW of 2 MW turbines are entering a repowering programme. Frankly, this is quite striking: we are talking about turbines installed mainly between 2005 and 2010, which are barely 15–20 years old. The fact that wind farms with G8X-2.0 or V90 turbines meet the eligibility criteria (>20 years) and, above all, have a business case for repowering ahead of schedule, speaks volumes about the level of incentive the government is providing. The economic threshold for removing a turbine and installing a new one is rising very rapidly.

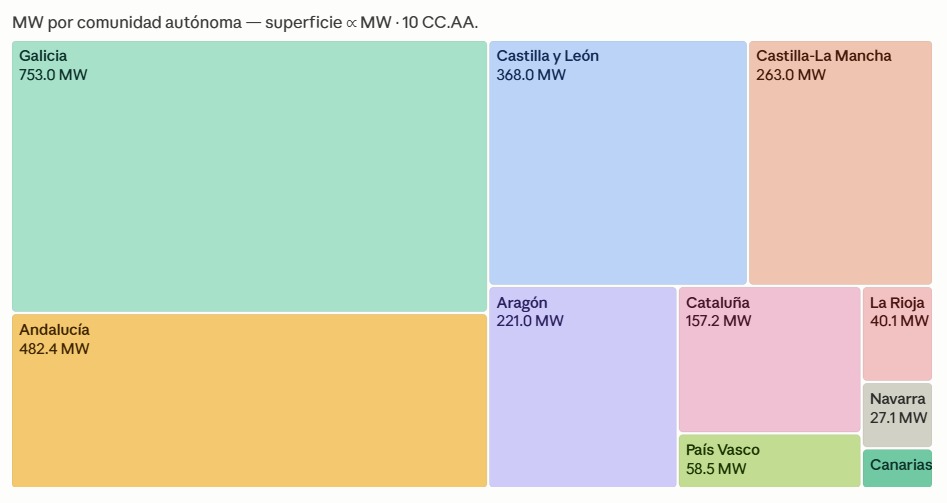

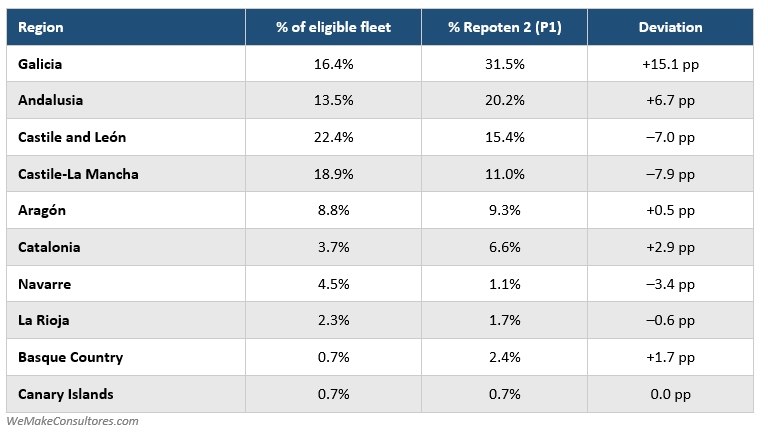

Geographical distribution: Galicia and Andalusia account for more than half the volume

The concentration of volume in a few autonomous communities is also striking. To see whether this concentration corresponds to the installed fleet, we have compared it with the eligible wind farm for Repoten 2 by region, that is, the total number of wind turbines connected to the grid before 30 June 2010. In Spain, this stock amounts to around 19.3 GW. Let’s see how this eligible fleet is distributed compared to the Repoten 2 allocation:

The most striking feature:

- Galicia is significantly over-represented, with 16.4% of the eligible wind farms accounting for 31.5% of the programme.

- Andalusia also appears to be over-represented in the allocation. This is likely due to the existence of older wind farms in Tarifa, Cádiz and the Strait, which are already well over 20 years old.

- Conversely, Castile and León and Castile-La Mancha appear to be clearly under-represented. They account for 41% of the national eligible wind farm capacity but barely 26% of the call for proposals. There are many old wind turbines in Soria, Burgos, Zamora, Albacete and Toledo that have not been moved.

This geographical concentration has significant logistical implications: the bulk of the work involving dismantling, transporting old blades and installing new turbines will be concentrated in Galicia and Andalusia over the next 3–4 years. This may be an advantage from an operational perspective, as dismantling teams will have to travel less and projects may even be able to overlap.

Who does this really benefit?

Let’s list the key players and see who comes out on top:

- Developers: clear winners. An average subsidy of €194k/MW on a typical repowering CAPEX of €1.3–1.5m/MW is a significant boost to speeding up the final investment decision (FID). Repowering without subsidies often has a tight IRR; with a 13% direct subsidy on CAPEX, the business case becomes viable.

- OEMs: manufacturers are largely indifferent as to where demand comes from. A contract for a Vestas V172 or a Siemens Gamesa SG 6.6-170 is invoiced in the same way, whether it comes from a new (greenfield) project or a repowering project. What is significant, however, is that almost all projects will use equipment manufactured in the EU, as this was awarded 10 points in the scoring system

- Dismantling and recycling companies: firms such as RenerCycle, which already has experience in projects such as Muel, Montes del Cierzo and Caparroso, will have many potential projects in the coming years.

- Crowdfunding: another aspect that was scored in the tender process was public participation. Companies such as Fundeen enable priority participation for residents of the municipalities where the project is being carried out, a scheme already successfully tested in the repowering of Montes del Cierzo.

Does this volume add to new installations or replace them?

In theory, it is in addition, as we are talking about different markets, but in practice the wind power sector faces very real bottlenecks. Logistical and manufacturing bottlenecks exist, but in the past we have seen that they can be resolved. However, there are others more related to project management and, above all, to financing, which are more complicated to resolve. Major developers have annual investment caps. Every euro allocated to a repowering project is a euro that does not go towards a new development.

In a scenario without these constraints, both approaches would coexist without issue. In the real-world scenario, repowering could divert some of the investment that would otherwise go towards new capacity. How much is difficult to quantify, but it is an effect that should not be ignored.

There is one final point worth raising. A repowering project does not deliver the same marginal MWh as a new wind farm.

When repowering is carried out, the wind farm usually ends up with a similar installed capacity, as the limiting factor is the grid connection. What does improve significantly is the capacity factor: new, much more efficient wind turbines capture the resource much better. The official estimate is that annual production doubles with a marginal increase in installed capacity (in the first round, there was an 8% increase in capacity with a doubling of energy).

But that ‘doubling’ is calculated on an outdated basis. If we compare this with a greenfield alternative, where each new MW connected at a new site adds ~2,500 MWh/year to the system, repowering clearly loses out. In a greenfield project, the increase starts from zero. In a repowering project, the net increase is the difference between the new output and what the old wind farm was already producing.

For the PNIEC targets (50.3 GW of wind power by 2030), what counts is the net new capacity. And in that regard, a repowering project that replaces an old wind farm with one of the same capacity contributes 0 MW to the target, even if it produces twice the MWh.

Conclusions

Repoten 2 is, without a doubt, an excellent measure from several points of view: it modernises the ageing wind farm fleet, boosts the Spanish circular economy, encourages local participation and reinforces domestic content through award criteria. It is a smart and well-designed tool. But it should be complemented by other tools to drive new installations and thus prevent what should be a complement to the main market from becoming the main driver of activity. German-style onshore auctions would be the perfect complement to Repoten 2 to ensure volume for both new installations and repowering.

energy-charts.info

energy-charts.info