Wind and solar PV in Spain – Overview of 2022

energy-charts.info

energy-charts.infoFor the fifth year, we publish a summary of how wind and solar power have performed in Spain in the year that has just ended. A year marked by electricity prices, but also by the spectacular take-off of photovoltaic solar energy, which seems unstoppable towards becoming the main source of national generation in just a few years.

The data for this report are publicly available on the excellent website of Red Electrica. Some of these data are still provisional, so they may vary somewhat when they become definitive, but they will be small changes that will not affect the overall picture.

-

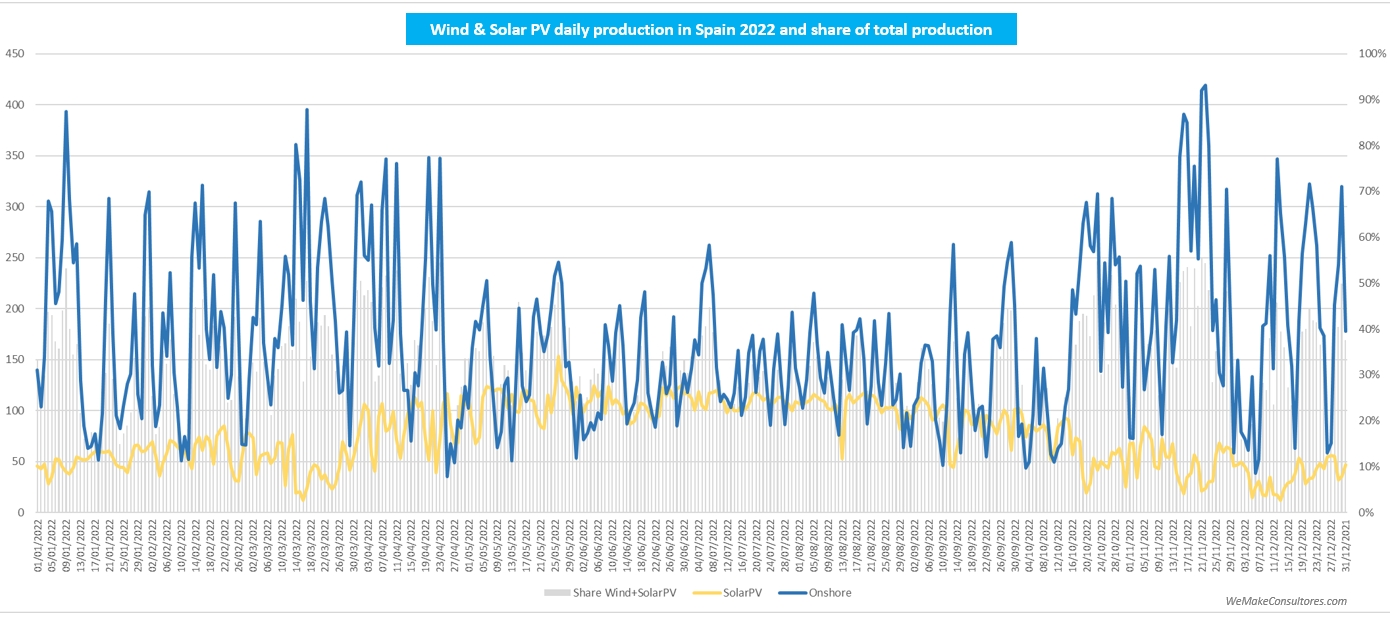

Daily production

- As usual when looking at this type of graph with daily resolution, it is impressive to see the great variability of wind power production, with peaks and valleys occurring over the space of hours. With the battery systems currently available with storage capacity of 4h at Lion and more than 8h at flow, we are getting closer and closer to the year when these saw teeth will disappear and will not be a grid integration problem.

- This year we have added bars to the graph indicating the share of daily generation covered by wind + solar PV. Specifically, on 21 November wind and solar PV covered 55% of the day’s demand.

- Wind generation reached its daily maximum on 22 November, with 419 GWh of production. That day also saw the highest combined wind+solar production with 443 GWh.

- Solar PV reached its maximum production on 26 May with 153 GWh, which is 22% more than the maximum in 2021.

- As for the minimums, the variation ranges of wind and solar are lower than in 2021, with wind remaining at 8.3% of the maximum and solar at 7.8% (vs. 4.5% and 5.6% respectively in 2021).

- Meanwhile, all renewables (including hydro and others) covered 63.4% of demand on 23 April.

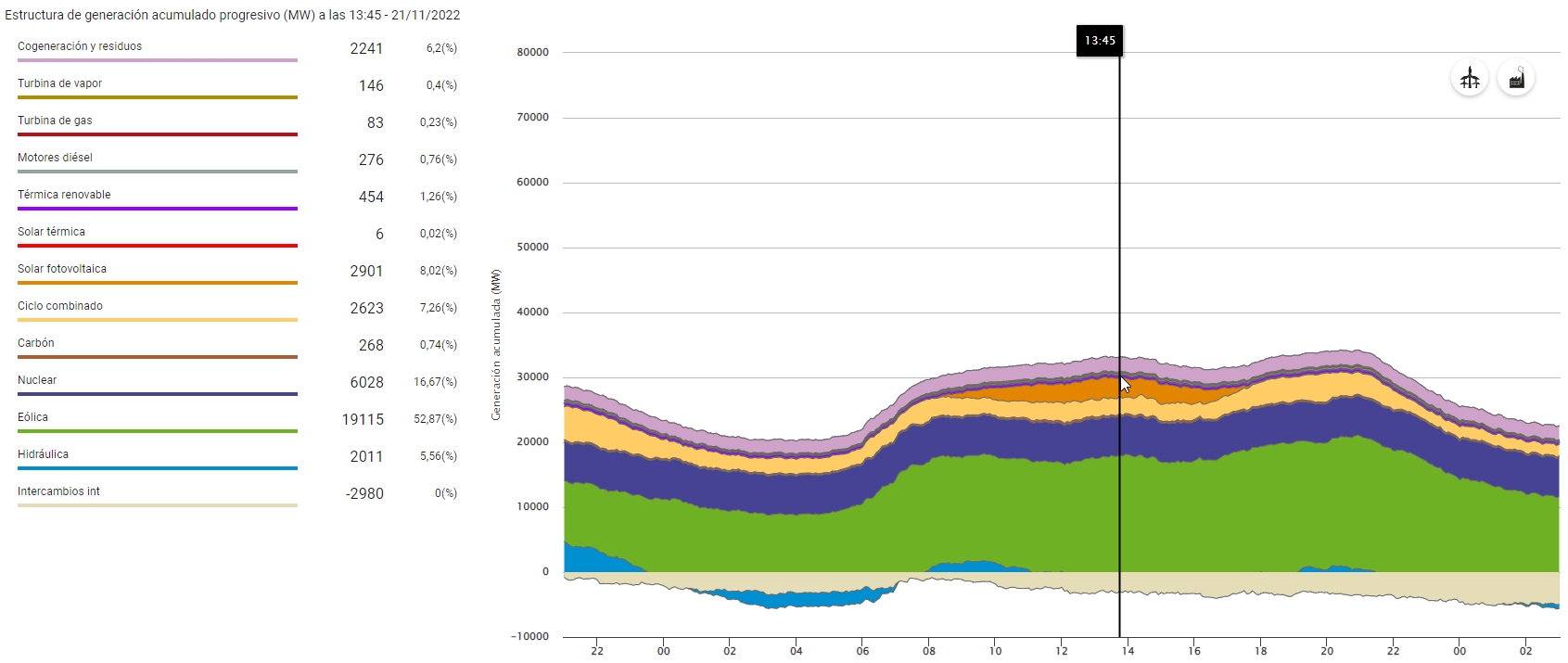

- A closer look at the generation structure on 21 November shows that at 13:45h, wind and solar covered 61% of demand.

-

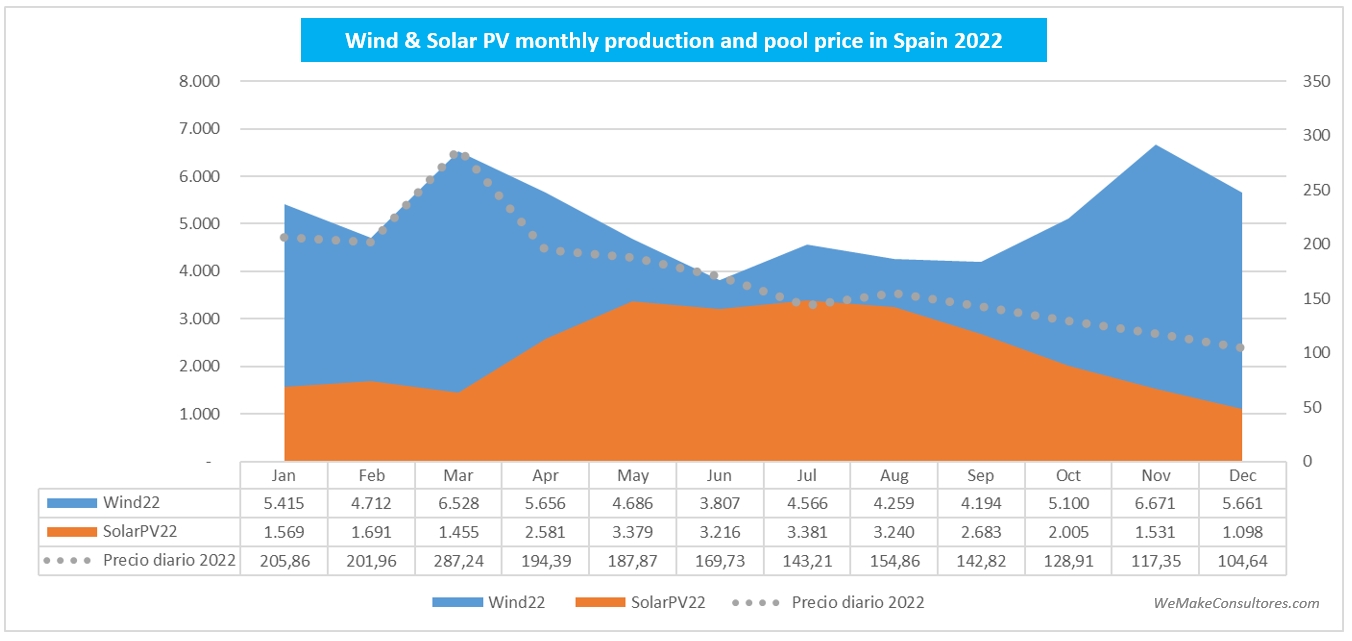

Monthly production evolution

- By representing the production data by month, the curves are much smoother and the great seasonal complementarity of wind and solar is much better appreciated.

- By superimposing the curves of previous years, the spectacular growth of solar PV can be seen.

-

Annual production evolution

- Solar PV was once again the main protagonist in 2022 due to its spectacular growth in annual production, with a spectacular 33% and becoming the 4th largest source of generation in Spain.

- Wind has not had a good year as its production has stagnated and has not been able to reedit its leadership of 2021.

- REE has already advanced the main data for the year in its recent press release, and it is worth highlighting the 3% drop in electricity demand. It is clear that the high price is the main cause, but I would like to believe that both efficiency and self-consumption are also helping to reduce connected consumption.

-

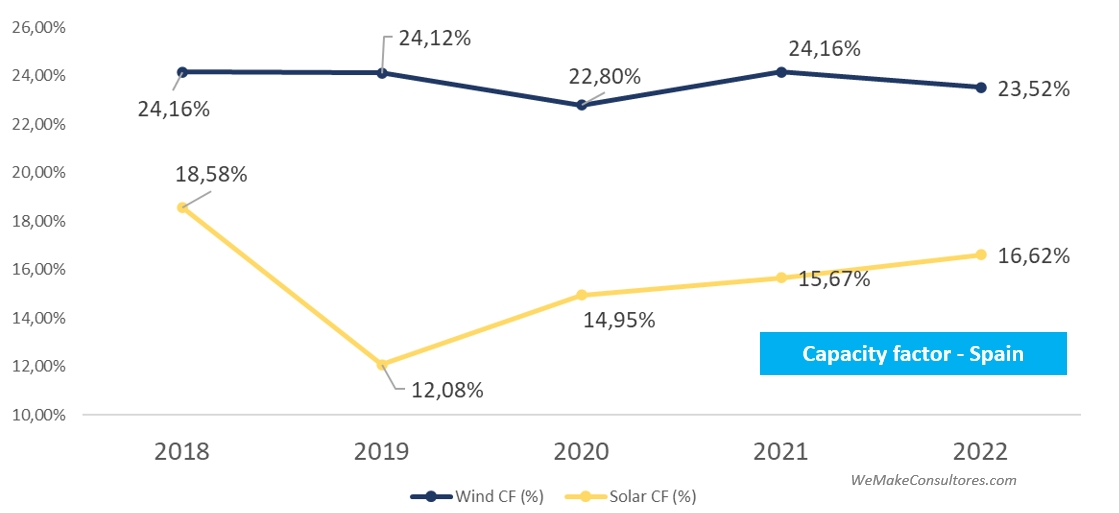

Capacity factor

- In terms of capacity factor, solar PV has also improved by one point compared to 2021, while wind has fallen slightly, a factor that has meant that annual production has not grown.

- It should be remembered that the main element affecting the capacity factor is the resource (wind and irradiance) available each year, but there are also other factors such as the efficiency of the technology, maintenance or curtailments. In general, with equal resource we should see better capacity factors as both solar and wind technology and O&M are becoming more efficient.

-

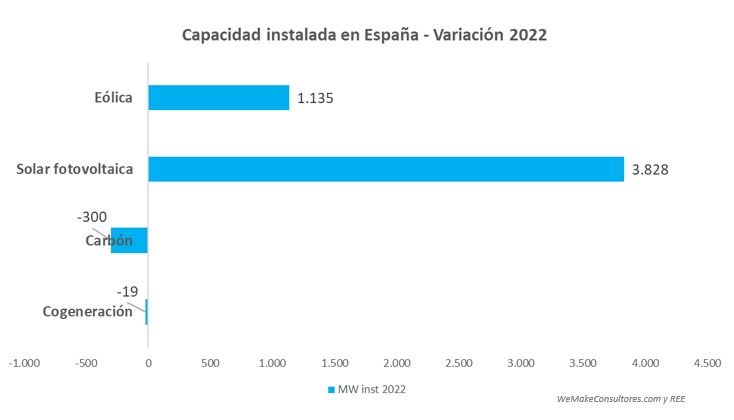

Installed capacity

- In terms of installed capacity, there is still no definitive data, but taking the data published by REE on its website, we can see that photovoltaic has grown by almost 4 GW, which is above the PNIEC targets. If we add to this the self-consumption installed this year, which could be around 2 GW according to some estimates, 2022 has been a record year for solar installations. And 2023 has started strongly with the sprint of DIAs taking place in January, so we will see these figures surpassed in the coming years.

- Wind for its part has improved on the 2021 figures but the 1.1GW installed is still a long way off the 2GW/year path set by the PNIEC. Let’s hope that the unblocking of the procedures will accelerate the pace of installations in 2023 and 2024.

- And as a happy ending, we see that the coal continues to be taken out of the mix and although only 300MW have been withdrawn (in 2021 there were almost 2 GW), it is still good news.

-

Market prices

- And now we come to one of the great protagonists of 2022: wholesale market prices. We started the year with average monthly prices above 200 €/MWh, but from March onwards, the measures taken first by the government and then by Europe to adapt the marginal market to the exceptional situation we are experiencing have managed to reduce the average price, which, although very high, has stabilised at around 100 €/MWh.

In summary, 2022 has been a year of lights and shadows for renewables, with some very positive aspects and others that need to be worked on in the coming years.

We are moving in the right direction, but let’s not deceive ourselves: we need more speed or we will not meet the 2030 targets. We need to speed up the processing of projects while increasing the positive impact of projects on local communities and without reducing environmental requirements, we need to accelerate the deadlines for offshore wind and storage must be a priority.