A Wind Airbus?

A few days ago, in the midst of celebrations marking the tenth anniversary of Acciona Windpower’s integration into Nordex, José Manuel Entrecanales remarked that “as Nordex’s main shareholder, I would vote in favour of a merger with any of the major Western manufacturers to create a ‘wind power Airbus’”. The idea is not new, but for the main shareholder of the second-largest Western OEM by market share to voice it openly certainly is. It is time to calmly analyse the feasibility of the proposal and how it might take shape

What exactly are we talking about?

It is worth putting what has been said into context. Entrecanales has not announced a deal, nor has he negotiated one, nor has he even suggested a preferred candidate. What it has said, in a conversation with journalists in Hamburg, is that consolidation is necessary to gain scale against China, that it sees five potential players (the four mentioned plus Nordex) and that its vote as a shareholder would be in favour “if the right circumstances were in place, with the right exchange and the necessary approval”.

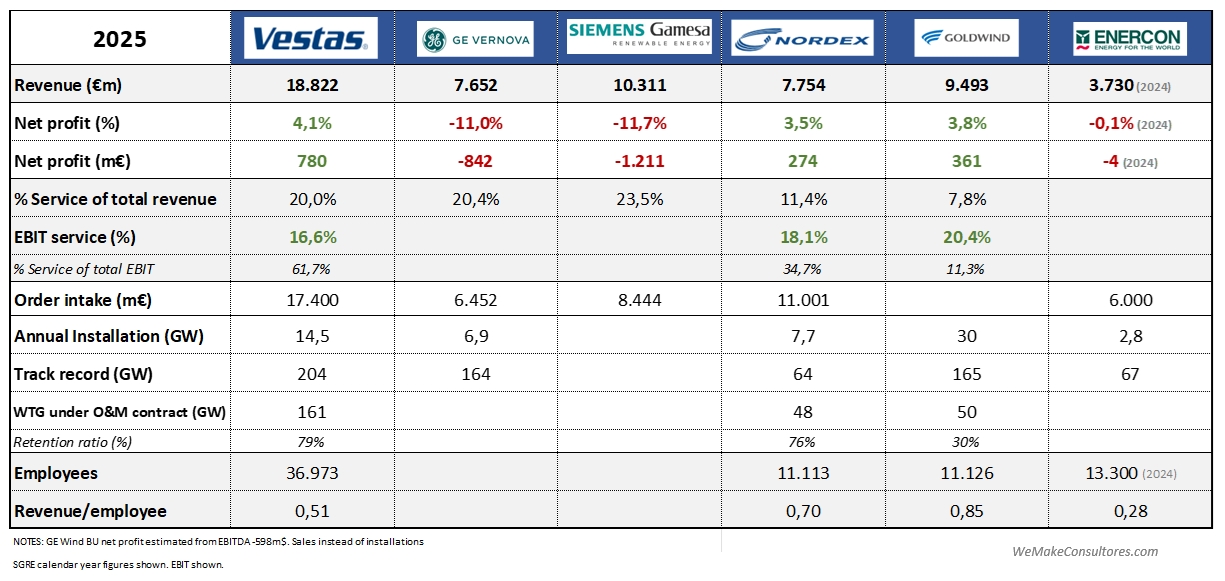

But the declarations of intent by the main shareholder (47.1% of the capital) of the manufacturer that already dominates 45% of the European onshore market are no small matter either. And even less so given the current context: a Nordex in top form, an SGRE trying to stem the tide of losses, a GE Vernova throwing in the towel on wind power, an Enercon which, although small, is in full recovery, and a Vestas more dominant than ever.

It could be a way of saying that Nordex is up for sale, but I don’t think it’s necessary to do so publicly and in that forum, so it’s clear there’s more to it than that.

The analogy with Airbus: nice, but…

The comparison with Airbus is the one used by Nordex’s own CEO, José Luis Blanco, and it has been picked up by all the media: “if European aircraft were manufactured by four separate manufacturers, there probably wouldn’t be any”. It is an analogy that has already emerged in the past within the sector and which we have even mentioned on this blog.

But there are some aspects that mean the Airbus case is perhaps not the best example, and the most relevant was public involvement. Airbus arose from a political decision, was created with public funding and was protected by regulation. In fact, the founding states remain shareholders to this day. “EuroWind”, as we shall henceforth refer to the potential wind power Airbus, would be a merger between 100% private companies and, in principle, would not have such clear public support, at least initially.

Another aspect that distinguishes the two cases is that Airbus was born in a rapidly expanding market, whereas EuroWind would be launched with a clear defensive focus and with little real chance of taking market share from Chinese manufacturers.

It is true that there are some similarities, such as the urgent need to cut R&D costs, unify the product range, and increase manufacturing volume and bargaining power.

Another example that is perhaps more appropriate (but less promising)

The 2019 attempted merger between Siemens and Alstom to create a European rail giant is a more recent—and perhaps more apt—precedent. The same argument (to curb the Chinese giant, in this case CRRC), an agreement between private companies, enthusiasm from the French and German governments, but no happy ending: Margrethe Vestager blocked it on antitrust grounds. The phrase that went down in history: “We cannot build European champions by undermining competition.” It matters because it sets a legal precedent regarding the competitiveness-competition debate.

It is clear that industrial mergers in Europe that create a dominant player will be very difficult to push through.

The candidates: a one-by-one analysis

But let’s get to what we like on this blog, which is to speculate and engage in a bit of wind-power sci-fi, and analyse the four possible candidates for a potential merger or takeover with Nordex.

1. Vestas: the impossible dream

It would be the mother of all deals. Combined, the new entity would be by far the largest Western OEM, with an onshore and offshore presence, an installed base of 270 GW and a hugely powerful services business.

Although there is significant overlap, particularly in Europe and in onshore products, the synergies are very attractive: Vestas would bring its offshore expertise, strength in the US and APAC, and a vast fleet, whilst Nordex would contribute its strength in Germany, Southern Europe and Latin America, its client/shareholder ACCIONA, and a highly optimised supply chain.

The problem is that Vestas does not seem to want or need a deal of this kind. Despite the enthusiasm of some Spanish media outlets, the company’s statements on the matter could not have been more lukewarm: “Vestas’ strategy is based on organic growth, but given our leading position in the sector, we will participate if opportunities arise”.

Vestas is the market leader, is clearly growing, has no history of major acquisitions, and its positioning as a premium OEM insulates it somewhat from the Chinese threat.

Probability: low. At present, Vestas has no incentive, and the Danes traditionally prefer to grow organically.

2. Siemens Gamesa: the “natural” fit, but a poisoned one

On paper, this is the most obvious option. It would address Nordex’s two major shortcomings: offshore (where SGRE is a global leader) and mature services with a huge installed base. Furthermore, SGRE’s perpetual crisis situation, coupled with pressure from certain shareholders, makes it the perfect candidate.

But Siemens Energy has stated on many occasions that offshore is a strategic business, so what would happen if the merger were only with the onshore division? Well, the overlaps would be enormous: similar products and technology, the same markets, a similar manufacturing footprint, and even Nordex’s management team with a Gamesian past… and to top it all off, Nordex would find itself with a business devastated by the crisis that would need to be revived with significant investment… it does not seem like the scenario ACCIONA is dreaming of at the moment.

Probability:

- Full SGRE: moderate. It seems the only option that makes sense, but it’s hard to see Siemens Energy giving up its offshore crown jewel

- SGRE onshore only: low. It does not look like a merger that will result in a ‘European champion’, at least not immediately.

3. GE Vernova: the divorce that almost signed itself

With all the offshore problems and Trump’s harassment of the business in the US, the feeling that GE Vernova wants to offload its wind division is growing, and this could be a golden opportunity

The complementarity is quite high. GE would bring leadership in the US, offshore experience and products, and a US customer base.

The problem is that GE remains a money-losing machine and I don’t think Nordex is up for taking on the risks. Furthermore, it would be a merger that wouldn’t even result in a leader in terms of turnover.

Probability: high that GE Vernova is willing to sell, but medium/low that Nordex will buy without some agreement that the warranties will continue to be supported by GE.

4. Enercon: the confirmed bachelor

This merger would create an absolutely dominant player in Germany. It could also offer two distinct technologies (direct drive and DFIG) to a very diverse customer base.

The problem is that Enercon belongs to the foundation left by Alloys Wobben upon his death and, if I recall correctly, one of the founder’s express wishes was that it should not be sold. I am unaware of the legal possibilities, but at first glance, it does not seem the ideal candidate.

Probability: very low, unless the shareholder family expressly wishes it (assuming there is a legal possibility)

A multi-pronged operation?

That really would be a bombshell. It is true that for it to resemble the ‘Airbus’ concept, we would be talking about a merger of several OEMs. We could be talking about an OEM with over 400 GW installed, a turnover of nearly €40 billion and 30 GW of annual installations… a giant that would strike fear into any Chinese manufacturer and would surely attract support from national governments and perhaps even the EU.

But having experienced the reality of a merger between two manufacturers that, in theory, was straightforward and offered huge synergies, I don’t even want to imagine what a three- or four-way merger might be like: different cultures, complex valuations, differing priorities, battles to maintain their products and technologies, internal power struggles…My impression is that, in these processes, the last thing on anyone’s mind is the customers and the market.

Probability: very low in a simultaneous format. More realistic in a sequential format: first a dual operation (Nordex + SGRE, for example), and then subsequent additions involving GE Vernova assets, for instance.

Operational aspects of the potential transaction

- Duration: it is not unreasonable to expect that it will take around five years from the announcement of such a transaction until the merger is fully operational. Whilst the legal aspects of the transaction can typically be finalised within 12–24 months, the internal reorganisation involved is often costly.

- Legal structure: this will depend on who the merging parties are. If it is a clear-cut acquisition, it will be a merger by absorption, but if the parties wish to structure it as a merger, the best approach would be to create a new company.

- Antitrust: this would be the real stumbling block of the deal. Focusing solely on the European aspect, it is clear that the European Commission, via DG COMP, will scrutinise the deal closely. If the merger creates a dominant OEM in Europe (which is highly likely given that Nordex is already the market leader), the only option left will be to play the ‘Chinese threat’ card.

And here, what happened with Siemens-Alstom is very illustrative. Vestager rejected the ‘European champion’ argument because no real Chinese threat to the European market was apparent (CRRC had never sold a train in Europe). In wind power, the case is similar: much ado about nothing. As we explained some time ago on this blog, the “Chinese invasion” remains more of a spectre than a reality in terms of actual market share. As Windletter explained a while back, only 7% of Chinese turbine exports are destined for Europe. Frankly, it seems unlikely that the EU would turn a blind eye to such a deal.

Is this really good for the sector?

This is where we enter uncomfortable territory. Because the real answer is: it depends on who you ask.

- For OEMs: yes. Less competition, greater bargaining power with customers and suppliers, higher volumes to recoup R&D costs, and the chance to focus on reliability and services rather than a suicidal price war.

- For developers and utilities: far less so. Fewer options, upward pressure on prices, dependence on a near-monopolistic supplier in certain segments. In the offshore sector, there are already complaints from the major utilities about the SGRE-Vestas duopoly, so a similar situation in the onshore sector would be very poorly received by the market.

- For the European supply chain: ambiguous. If consolidation is accompanied by commitments to local manufacturing, that’s good. If it’s to optimise costs with global platforms manufactured in Asia (as Nordex already does with its hubs in China and India), that’s bad.

- For Europe as a continent: probably good, if done right. Having a pan-European champion in a technology considered strategic, with control over software, maintenance and updates (an aspect on which Entrecanales insisted), is what Draghi recommends and what industrial sovereignty dictates.

Conclusions

My impression is that for this operation to truly be a game-changer, it needs to involve multiple parties, as I do not believe a merger of just two (without any other players) will change the landscape significantly. And as we have seen, an operation involving several parties that is not sponsored and driven by the institutions is highly likely to be scuppered by the bureaucracy in Brussels.

But beyond operational details, it is very positive that the debate is being brought to the table, and hopefully this debate will be structured around medium- and long-term strategic criteria rather than corporate emergencies. The objective should be clear: to have a strong, profitable and competitive European wind turbine manufacturing industry.